Interledger, a protocol for the future of money

The Challenge of Global Payment Systems

Alex Lakatos introduces the complexities of global payment systems by recounting personal experiences with international transactions. He highlights the difficulties of transferring money across borders due to banking regulations and the lack of interconnectedness among banks. Lakatos uses examples such as the sanctions on Pakistan and his own challenges in sending money to Romania to illustrate the inefficiencies and high costs associated with current banking systems. This segment sets the stage for discussing potential solutions to make global payments as seamless as sending an email.

Designing Interledger for Seamless Transactions

In this segment, Alex Lakatos discusses the development of the Interledger protocol, inspired by the architecture of the internet, to facilitate seamless money transfers. He explains how Interledger aims to replicate the internet's layered structure to connect disparate banking systems. Lakatos emphasizes the challenges of integrating with outdated banking technology and the necessity of creating a user-friendly interface that resembles a web address for financial transactions. This approach aims to simplify the complex process of transferring money between different banking systems.

Implementing Interledger and Overcoming Technical Challenges

Alex Lakatos delves into the technical implementation of Interledger, highlighting the creation of a robust accounting ledger capable of handling high transaction volumes. He describes the development of Tiger Beetle, a resilient ledger system tested extensively to ensure reliability. Lakatos discusses the limitations of existing banking infrastructure and the need for a modern solution that can support real-time transactions. This segment underscores the technical innovations required to make Interledger a viable alternative to traditional banking systems.

Innovations in Payment APIs and Web Monetization

In this segment, Alex Lakatos explores the development of open payment APIs and the concept of web monetization. He explains how these innovations aim to simplify transactions by reducing the information required for payments and enabling microtransactions. Lakatos introduces the idea of streaming money, allowing users to pay for content consumption in real-time, which contrasts with traditional ad-based revenue models. This approach encourages content creators to focus on quality and engagement rather than click-through rates.

Regulatory and Legal Challenges in Financial Innovation

Alex Lakatos addresses the regulatory and legal challenges faced when implementing financial innovations like Interledger. He discusses the complexities of navigating compliance and legal agreements, highlighting the significant role lawyers play in the process. Lakatos shares experiences from working with regulators and legal teams, emphasizing the need for collaboration to overcome these hurdles. This segment illustrates the importance of regulatory understanding and legal frameworks in the successful deployment of new financial technologies.

Call to Action for Building the Future of Money

Concluding his talk, Alex Lakatos makes a call to action for collaboration and innovation in the financial technology space. He invites developers, regulators, and financial institutions to join the effort in transforming money transfer systems to work like the internet. Lakatos emphasizes the long-term nature of this endeavor and the need for a collective effort to overcome the challenges ahead. This segment serves as an inspiring conclusion, encouraging audience participation in the ongoing development of Interledger and related technologies.

It's a lot to follow and a lot of trends in here where you build protocols in our products.

That's why we tried to figure out a simple problem.

Actually, we didn't try to figure out a simple problem.

We had a problem, so about 10 years ago.

I dunno if you remember Pakistan and the US had the little love quarrel.

Then the US put Pakistan on the sanctions list, and that meant we couldn't pay our designer that was based in Pakistan, designer who had nothing to do with this.

And like a few days ago, John ran another conference, which I happened to speak at, and I tried the little exercise on stage.

So 10 years later I tried a little exercise on stage.

I'm not on any sanctions list.

I was here in person and I asked.

The audience that tried to pay me to make it easy for everyone, I gave them all my banking details on three continents, right?

How many people do you think managed to pay me out of maybe 300 people in the audience?

200 people in the audience?

I'll tell you who managed to pay me.

The one guy at the back of the room who ran down the stairs with cash as the only person that managed to pay me.

And I made this super easy, like I have, I am in the fortunate, unfortunate position where I have bank accounts on three continents.

Sadly not on this continent because I don't live here.

So all of this is because in today's world, if you're trying to pay someone, you have very limited options.

It would be easier and cheaper in some cases to put money in a briefcase hop on a plane and hand over the money to another person then to actually try to pay them by bank.

And that's because in the banking world, all of your money.

No matter where you hold your money digitally, at the end of the day, your money lives in a bank account.

Even if it's in crypto, even if it's in whatever.

At the end of the day, it's still a bank account underneath.

You just don't see it.

And that means whenever you try to pay somebody, eventually the money moves between banks.

And if you happen to be within the same bank and you're trying to pay someone super easy, probably takes you about a minute or two depending on how good the internet banking app is.

And that is because money never actually physically moves.

Money lives on a ledger or an accounting ledger, and that one moves from a credit here to a debit there, and it's done.

If you're trying to do this.

Between two actual banks.

It starts becoming more complicated if the banks are in the same country and if it's one of the fortunate countries that are connecting all the banks together.

So out of about 200 countries in the world, 70 of them are only connecting all the banks together.

This one actually does, you've seen pay id, I think that launched recently.

And that's an instant payment system that connects all the banks together so they can transact.

So if you are lucky to be able to be connected, then the transfer might happen within 10 minutes later let's say.

If that's not the case, if the banks are in different countries, you start to run into a lot of, if this, then maybe, if not, then tough luck.

And that is because in order for money to flow, you need to have a relationship or a connection.

If two banks are connected, money flows between them or money teleports between them.

If you are part of, or if you're trying to move money between countries that don't really talk to each other.

So for example, I am Romanian.

I've left Romania, I dunno, maybe 10 years ago.

My mom still lives in Romania and I've lived in several different places.

Recently in the uk me trying to move money from the UK to Romania for my mom's birthday.

My mom's birthday was the 22nd of November.

Took me exact exactly seven days.

So this morning my mom got money and I lost about 18% of it.

And that's because even though they technically are in Europe, even though one of them left the European Union, the banks of Romania are not connected to each other.

They're also not connected to the European transfer market called zpa.

The UK left the European Union, so they got kicked out of sepa.

And so my bank in the UK has a relationship with a bank in Germany and they moved the money to Germany and that bank in Germany has a relationship with my mom's bank in Romania.

But all of this had to happen with two humans looking at that transfer and saying, who's this Alex person and who's this?

My mom's name is Carmen.

Who's this Carmen person?

Oh, they share her last name.

There's something funky in there.

Why is he sending her 50 euros for her birthday?

And so to solve this problem of humans and complicated routing algorithms between banks that require, telephone and a human.

Somebody said there has to be something better than this.

We've managed the root information around the world.

We've managed to connect networks of computers.

Why can't we connect this network of money?

How hard can this be?

Spoiler alert, it's eight years later and it's still a bit complicated and I'm gonna show you because we wanted to make sending a payment as easy as sending an email, right?

Somebody figured out email does the Fed verse in the world.

Why couldn't we do this to money?

And we realized there is a lot of.

There are a lot of structures and infrastructures in place that have figured out how to do networks and network effects to transfer things from one side to the other.

Most importantly, something that's been around for a few, for a few decades and that has worked out well is the internet.

Which takes this livestream, hi livestream is actually a lot of data packets broken down and shipped across networks of computers on competing routes.

Reassembled at the end, somewhere around the world sees me right now.

So we looked at the design of the internet and said, how can we do this to money?

The internet technically has five layers.

There's a application layer that everybody builds on top.

There's a transport layer with competing different protocols.

The underlying.

Thing that binds everything is actually the IP protocol, the thing that makes it easy to address people around the world.

And then you've got a lot of physical devices.

I think there's a talk happening after me that's gonna talk a little bit about how the internet actually works underneath, but you've got a lot of physical devices that let you connect to the internet, and then you've got, if you really care.

You've got the massive amount of submarine cables and satellites that actually connect these physical devices to have a global network.

And we tried to replicate this model for money.

We called it interledger because.

Internet is inter network banks work on accounting ledgers.

So we thought inter ledgers, that was a bad naming decision because crypto came along and now when you hear ledger, you think crypto.

Sadly, there's no crypto here.

Something half my job is traveling the world and the other half of my job is talk to the crypto bros and convincing them Intel has nothing to do with crypto.

It's funny, but it's a true story.

It's sad for me.

Yeah.

So we try to replicate the same principles of the internet.

We created the same layers.

We figured out how they fit together, how to connect from one bank to the other.

The problem with banks is not only that they are entities without an IT person, system, or developer on staff.

So we had to figure out how to talk banking.

The problem is even when, like all of the systems that run in banks are probably 40 years old and written in cobol.

So trying to replicate and put internet on, it meant we had to be very inventive and we had to have a lot of options about how to actually link into banks.

But we started thinking about the user first and the bank later.

One of the things that you've probably noticed on one of our slides is I have bank accounts on multiple continents.

All of them look different.

All of the account information looks slightly different.

One of them loses a long ass number called iban, which is an international standard only adopted by about 90 countries out of 200.

The other one is a sort code and account number, which is a UK specific thing because why not be special, and then the American system.

That uses three points of reference because anti-man monitoring is a problem and because the system hasn't been touched since Reagan was in office.

Yeah.

So we figured out what do you and I, people who live today.

Can easily understand or recognize, and we realize that's URLs, that's a web address.

So we've made money function like a web address, so you have an easily recognizable address for grandma, which is dollar domain name slash user identifier.

In my case, that's ILP dev slash triple zero, and we realized machines needed a way to interpret that dollar sign, so the dollar actually converts to HTPS.

And that is our user facing layer or application layer that everybody's building on top of.

We had to figure out a way how to move this money, or how to make this money actually move.

Turns out the internet does something really smart if that is congestion on the network layer.

It breaks down packets and sends it across multiple routes to hit the destination.

If you lose a packet, because the network is slow, you just send that packet again on a different route, reassemble it at this destination tadda.

When you try to do this with people's money and you lose a packet of money, people tend to get upset.

So we had to create this protocol, this transfer level protocol that basically broke down a payment in multiple packets.

Scramble them around, streamlined all of them, and then send them across the network one by one at the speed of the internet.

The thing is, if it does not get to the destination, it's not lost.

It has a self-healing mechanism that reverts back to the sander.

So there's no way to lose money in this process.

We figured out the other problem with packetizing payments and making two ledgers talk to each other is they represent currency in exactly the same way.

So the Australian system represents money as 10, and that 10 means 10 Australian dollars.

The UK system represents money as 10.

The problem is that 10 is actually 10 British pounds, and nobody can figure out the exchange rate between them because the ledgers don't talk to each other.

So we've designed the protocol layer, the packet to contain all of this information needed to send money from one ledger to the other in a way that the receiving ledger could actually understand what that is.

And that means we have a destination and amount.

And on top of that, we have execution data that says, Hey, if you didn't get there within a minute, you are lost, come back.

In order to make all of this happen, we had to figure out a way to connect the layers or connect the ledgers, link them together.

We have multiple ways, but the most popular one is probably BTP, and that's because we looked at not only how the internet works, the internet is actually not bilateral.

The internet is single connection.

You plug a cable and that cable automatically is always, but the banks don't really work that way.

If you look at some of the other mining networks like Swift.

That work on bilateral agreements, they work unilaterally.

So while I like John and I trust John, I have a connection to John, but John doesn't really like me and doesn't really trust me.

So he's never gonna send me money.

I'm comfortable sending him money.

He's never comfortable sending me money.

So we have to figure out a way to make this connection or to codify this connection with money where.

If you're a small bank, you'll trust the big bank and you'll send it money, but the big bank won't trust the little bank, and so the money only flows one way.

Because we had to explain all of this to banking people, eventually we figure out how to map this to what banking is today, which is, there's a messaging phase where you agree on terms, and then there's a cleaning phase where the money leaves from one end, but didn't really get on the other side yet.

You do all your checks in between.

That's why a transfer can take up to seven days because that clearing process basically clears the money to arrive and then the settlement layer, which basically means you've taken it out of one bank you've deposited in the other bank, and now the money is really there.

For us, we realized that it was impossible to do settlement for most people because if you think about it, if you really wanted to give you money now, and I wanted to use it.

In the real world, you'd have to settle in cash.

We'd have to settle in cash.

We'd have to agree on terms, and then you'd have to gimme cash.

The banks, some of them do this in gold, some of them do this with armored trucks, and some of them do this with trust relationships.

So we have to decouple the settlement rails from everything else messaging included, because otherwise a transfer wouldn't actually complete in a timely fashion for a human to actually use it.

And so this is a good idea based on the internet.

We released the protocol in 2016.

It was a great idea.

The problem was, it was just an idea.

It was just a bunch of words on a piece of paper.

So we said, what happens when people try to implement this?

And we actually saw what happens when people tried to implement this.

It took them 18 months as a bank to get this into a any usable state.

I think about four years ago, we realized that any great idea, it needs a lot of help, a lot of work.

So we started building tools for it.

We built our own reference implementation, trying to help people build faster or adopt this protocol faster.

I think when I joined the adoption rate was 18 months if you were really good and today 2024 the fastest adoption of Interledger has been seven days from, yes, let's do this to, we have a working implementation seven days, and that's because we built all the tools you need in order to make it work.

Now, seven days was a very fortunate scenario.

I would be happy with a month.

If you make it in under seven days, if anyone works for a bank, I think I met somebody from up recently.

If you're at up, you're in the room and you want to try this out and you make it in under seven days, I would buy your weight and beer.

Yeah so on top of having to implement all of this ourselves so that other people could use it, we realized modern technology is not set up for banking.

And that is like the accounting largest bank queues are literally 40 years old, I think in the pandemic.

The city of New York was paying half a million dollar for a COBOL developer because the New York infrastructure is written in COBOL decades ago, and they couldn't support people staying home and trying to pay over the internet.

So they needed developers to develop a system that was 40 years old.

We instead of trying to borrow that system we thought we could do better.

And so we said MongoDB.

The database of choice for developers today was gonna be good enough.

Turns out it wasn't.

So a country like India does about 70 billion transactions a year, maybe a hundred billion transactions a year, but the transactions aren't linear.

The transactions happen regularly through the day on an effect.

But if it's the 28th of November, Thanksgiving, black Friday, there's a million transactions happening instantly.

Everybody tries to process, like everybody tries to buy things on a curve.

Everybody gets paid on a curve, so there is actually congestion in the system.

Visa and MasterCard, some of the current payment networks in the world support 60,000 transactions per second.

Incidentally, like the same amount like Mongo DB does.

And if you're gonna try to buy something today, I think one of the speakers tried to buy something during the talks.

If you're gonna try to buy something, the money never leaves your account the moment you hit pay.

I dunno if you've noticed your card is gonna get charged maybe tomorrow, maybe two days from now, maybe three days from now.

And that is because they cannot actually handle this many people trying to buy something over the internet.

So what they do is they save the card information on file and then they start processing it when the system is, middle of the night type of thing where there's no activity on the system and it takes them for a single day of shopping or two days of shopping, it takes them about five to finish processing.

So we had to create our own accounting ledger in order to support this because our team is in South Africa.

It's called Tiger Beetle.

Because it's the most resilient beetle on earth.

And we've spent considerable amount of time with the Apple team.

Apple has this time traveling debugger built on cloud where they change the speed of the clock of the processor and they can compress time so that a year of testing equates to about a hundred years of testing.

So for the past year and a half, that's 150 years of testing.

They've tried to break into the accounting ledger and they have a magnitude.

That's why it's the most resilient on the most resilient ledger right now.

That can process a million transactions per second.

We figured out a million transactions per second was enough to handle a country the size of India trying to send money from one place to the other.

And we thought we were done.

We thought, oh, we have a ledger, we have a reference implementation.

What more can we need?

Turns out it's good to have all of this, but if you require a math PhD to move money on the system.

It didn't really work out.

If you think about the banks today, or if you think about banking in here today, there is a new banking standard called open banking that allows you to access somebody else's bank account to move money or to see what's in the account, to see transactions.

It's a very good idea, a very poor implementation because in order to get access to this one little API, like any developer can use, you have to be accredited with one of the, I think it's called aka.

So you have to be an accredited person in order to use the API because there's no safeguards on the API.

So if I give you access to my bank account, I have to really trust you that.

You know what you're doing.

Turns out the regulator doesn't really trust people to know what they're doing, so they've imposed this regulation or limitation on it because we didn't want to do the same.

We've added a new layer of delegated access onto account.

In order to do that, we had to work with the people who created AUF.

To authenticate into accounts, to figure out a way to authenticate into resources.

So if you think about money as a resource, we can now portion out money as a resource and then delegate access into that.

For example, I can give you access to $5 from my account for the next two minutes, which basically means I've bought something from you so you can take the money and do whatever you want with them.

Or I can give you money to $5 every month out of my account because I subscribe to something.

Or because you're a digital wallet or you're Apple Pay, and I trust you to pay out of my account, you can have access to $200 out of my account for as many transactions as you want for the rest of the month.

All of this.

All of these technologies, cutting edge, bleeding edge technologies, we realized it was really good and a bunch of developers could use it, but you still had to have a lot of knowledge and a lot of interest to do and we figured out a way to make things simpler.

Even the banking APIs, they have so much power and so much relies on your account that we didn't think you should be trust, everybody should be trusted with this because at the end of the day, what most people need is payments.

So we took the banking APIs and we created a very, small subset of the API that's specifically designed to pay people.

And we've tried to make it so that you can use this Lego piece to build an easier user experience for when you want to pay.

Think about paying with a card today.

If you're trying to pay with a card, you need four pieces of information.

You need the long virtual card number, you need the expiration date, you need the CVV, and depending on the transaction size.

If it's below $50, usually you don't need anything else, even though you have to input your name because everybody asks for a name.

The name doesn't matter.

But if it's over $50, you'll see the requirement address, and that's because you don't actually need the whole address.

You need the postcode in the address to make a card transaction.

So we try to make it so that the only piece of information you needed to make a payment via the API was the account number.

So this is how it looks like if you've got an intelligent enabled wallet, you'll get the payment pointer somewhere on, you'll get the payment pointer somewhere on the, page for our wallet.

It's front and center.

And then you can use that payment pointer to get something.

I think I'm, I can't remember what I'm buying.

I think I'm buying courage here.

When I was doing this, when I was doing this video, I was a bit nervous about my talk because I'm the only, I'm the only thing standing between you and the coffee break.

Yeah.

So I bought card.

Oh, I bought lock as well.

So once you pay with Interledger, you just need the payment pointer and that's it.

And because we use delegated access, the shop actually takes you to your bank and says, Hey, I want to get money out of Alex's account.

Will Alex let me get money out of his account?

And that was it.

We made it, open payment APIs make it as easy to pay as you can.

When we built all of this was the intended use case.

We ma wanted to make payments as easy as sending an email, and I think that achieves it.

The thing that happened is we were a victim of our own success now, a victim of unintended consequences because we build this on modern technology and because we can support a million transactions per second per bank.

There is no more limitation to the card networks, because they only support 60,000 transactions per second, they have to limit the transaction size in order to limit traffic to the network.

So if I try to pay a dollar today, that is the minimum amount I can pay on card networks.

Out of which about 30% gets lost in fees.

They would want to support less than a dollar, but they can't because the infrastructure they're built on does not allow them, because we have the infrastructure.

We've basically said you can transfer as little as the hundred part of a cent, and that is only because it's a technical limitation.

The hundred part of a cent is nine decimal points.

We couldn't represent 10 decimal points reliably, so we said if you can represent it with nine decimal points, you can move it on the network.

And because we did that, we allowed the network to.

To perform this way.

A bunch of people figured out you can stream money if you can make a transaction every second, or a transaction every 200 milliseconds.

What's from stopping you of making 10 transactions per second?

A hundred transactions per second.

And Marcus is here.

Marcus.

Marcus wrote part of the spec, wrote the first version and the second version of the spec, I think.

Yeah.

So a bunch of people.

Figure out you could stream money.

What if instead of watching your website, I am not forced to watch ads in the process.

I can pay you for every second I'm on your website.

Instead of watching ads.

Why?

Why is that important?

Why is that important?

Ads actually incentivize you to take users off your website as fast as possible.

Whereas if you create engaging content, the users could actually stay more on your website.

And I tried out this theory, I was like impossible.

I should be able to put advertisements on any website, right?

I went to AdSense, and when you go to AdSense, step one, when you try to get an account is not actually get an account with AdSense.

And step one is build the right type of website.

And that is because AdSense or ads in general do not like it when users stay too much on a page, they like it when users get bored, click on the ad and try to buy something.

So Web Monetization works on the counterculture of that.

What if you could be incentivized for great content?

What if you would be rewarded for not spamming people or creating engaging content?

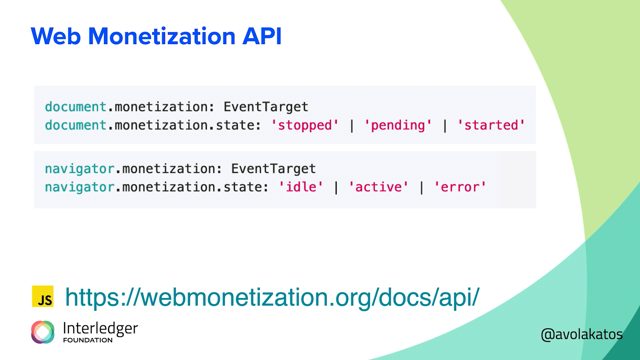

So the way does the way Web Monetization works as a publisher is you put a single line of code in your website and now you signal the ability to receive money.

It works from the same payment point that like everything around interledger.

It's baked into, or it's gonna be baked into the browser.

Because getting a new browser standard approved takes about seven years.

We couldn't wait that much.

I think we're in near three of the seven year process.

So we created this web extension for users to use Web Monetization without having to wait on a browser.

It's a simple setup process.

I try this out by trying to get my grandma to sign up.

I haven't managed to get there.

Grandma didn't manage to sign up.

But I think on a most people basis, you can put an accounting, you can put your account information there, you can figure out how much money you wanna spend, and then you start paying websites that are monetized while you, watch the content.

As I was saying, this is a seven year process.

We are in the seven year process or more that takes the standardized with a worldwide web consortium.

We would like feedback on this.

I think this is version two of the Spec, which was written three years ago, probably three years ago.

So we started the second version of the spec about three years ago.

It hasn't been touched since.

We choose to believe that's because it's stable.

I don't think it's that stable.

I think we need more eyeballs on it.

So if you have ideas, opinions, if you want this to work differently, we're open source.

It's out on GitHub and we highly encourage feedback.

So we figured out how to do all these things, right?

We figured out how to send money between accounting ledgers that were never designed to talk to each other.

We figured out how to connect a bank in the US with a digital wallet halfway around the world and make their users get money in real time.

We figured out how to make small payments and improve the user experience, and we thought everything was good in the world.

We solved for the problem we were trying to solve how to send money, how to make sending money as easy as sending an email.

And then we realized all of this technology we built, it took us about a bit of time, had one giant bottleneck.

There was a human, there was a human between technology and other humans.

It depends on where you are in the world.

If in a country like this, the human that is the bottleneck is the regulator, you have to explain what I did here and how long did it take me?

20 minutes, a bit over 20 minutes.

You have to explain this to somebody who's in the Central Bank, not exactly a tech savvy person that was born in the forties maybe if you're lucky.

We have had some successes with central banks.

So in parts of the world, there are whole countries that are adopting Interledger because the central banks highly innovative.

They get it.

They see this problem within their own network, so they're highly incentivized to adopt it.

Honestly, I thought talking to regulators was gonna be the biggest problem because you really have to explain it like they're five.

Or 50.

But I was so wrong.

I was so wrong it's not even funny.

The human, that's the problem is usually not the regulator, the human that's the problem is usually a lawyer.

And before I start talking about lawyers, do I have any lawyers in the audience?

Come on, don't be shy.

No lawyers in the audience.

Okay.

Thank God.

Okay, so the human does the problem is not the regulator.

The regulator will understand.

The regulator will see the value and will go, okay let's go for it.

The human thats the problem is the lawyer, because the lawyer will try to think up a million different ways this is gonna fail horribly and a million different ways this is gonna bite them in the ass later.

So for context, we've spent the last six months with the country of Jordan, with the regulator implementing this and trying to go live.

We have spent the same six months with 24 lawyers trying to get a simple piece of paper together that said, we agree to turn this live between a little digital wallet in the US and a little money transmitter in Europe.

Not even the same scale as the whole country, right?

We are going live with the country of Jordan, and the lawyers couldn't even meet in the same room to be able to draft the first piece of paper, the first agreement, because we're dealing with money and we're playing with banks and central banks.

We work in the regulated space.

In order to join intelligent or in order to connect to the intelligent network, technically you can do it in seven days.

Practically, you have to have a money license that powers your digital ledger.

So banking license, electronic money transmitter, money servicing business, whatever, some sort of license, and then you have to convince your compliance team, which is all lawyers, by the way.

That's what compliance means.

You have to convince your compliance team to meet with the other compliance team and define acceptable risks.

The kicker is because we're using cryptography under the hood, there is no risk in the network.

But the lawyers have to agree that there's no risk between trusting the other counterparty and like mitigation scenarios that we're dealing with after six months are what if the CEO of our partner bank decides to be a bad actor overnight?

Or what if the disaster recovery plans that we have in place, which basically means unless a meteorite strikes cert that data is protected.

What if those fail?

And that is, we've tried to build this thing in the desert and we've tried to make people come and we thought if the, if we build it they'll come.

But what we found out is.

Unless we start building a lot of roads for people to actually get there, nobody's gonna come.

And with that, I would like to make a public call for road builders.

We are a nonprofit with a team of about 50.

I think we need to be about 50,000 to actually make this work.

So if you're here and you have a desire to make money behave like the internet.

Join us.

We're open source.

We're in on GitHub.

We have a lot of work ahead of us.

We're in probably the sixth or seven years of a 20 year problem.

The internet doesn't, didn't happen overnight.

The internet for money is probably gonna take a little longer because lawyers are involved.

And with that I really, truly thank you.

Digital money has taken on a rather bad reputation of late, but what if the transfer money could be as frictionless, and inexpensive as the exchange of information enabled by the internet? Just as TCP/IP transformed the way information was exchanged, and drove the cost of that transfer inexorably lower, the interledger protocol, a W3C standard, aims to do that for payments and the transfer of value.

Already connecting traditionally unbanked communities into the world’s financial systems, the protocol opens opportunities for new business models and value exchange.

How might it transform what we do online and in the physical world?